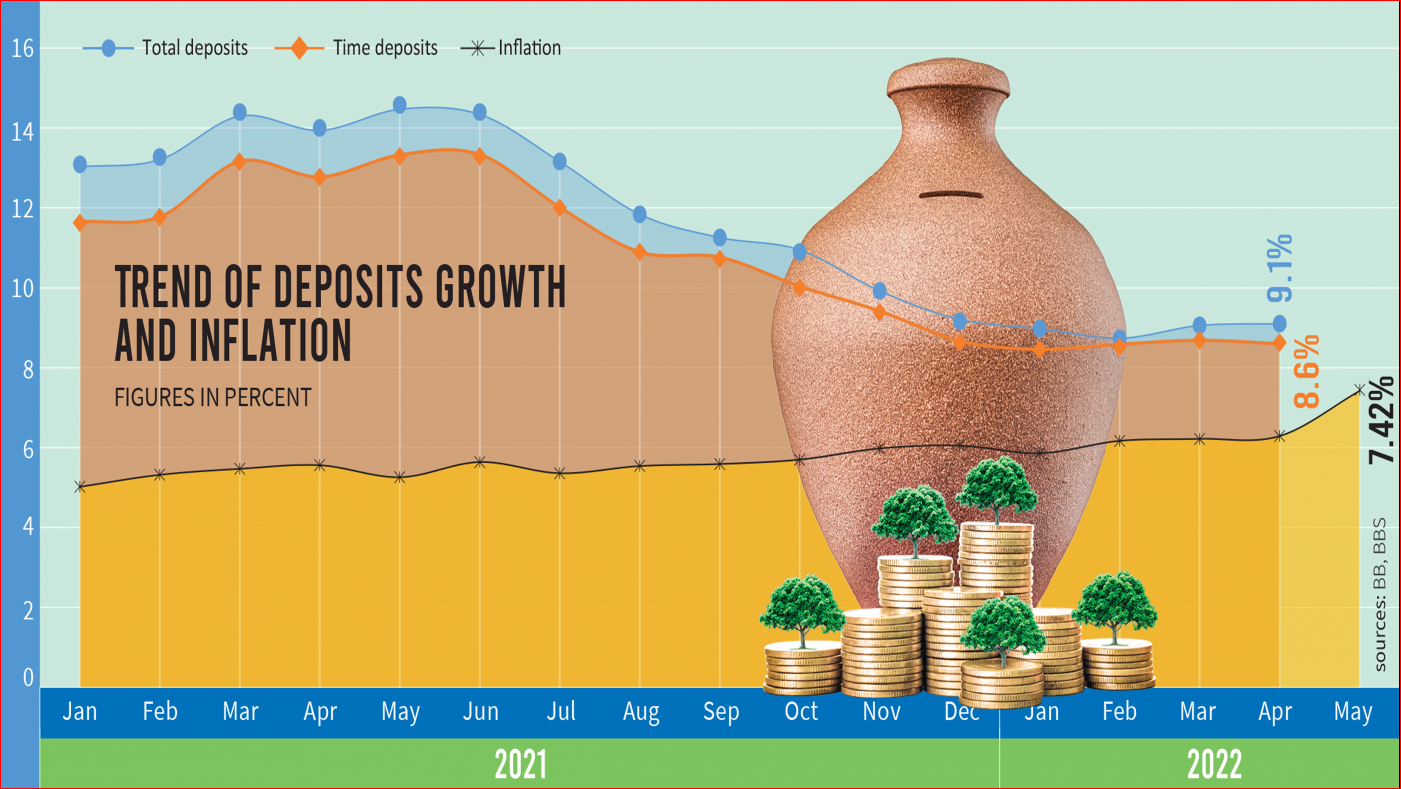

High cost of living has recently become insufferable for many, particularly for the common man and the people of the fixed income group. High inflation is eating into household income as the gap between income and expenditure has widened too much. This forces people to draw down or even encash prematurely their savings despite rising interest rates. Survival for the common man has become so arduous and tough that bank deposits and government savings tools, once seen as a secure refuge, are losing their appeal because people struggle hard to make both ends meet.

According to a report run by a local English daily, the country’s inflation rate for about three years hovered around 8 percent, with food inflation remaining above that mark for the past six months. According to the Bangladesh Bureau of statistics (BBS), the prolonged and obstinate price surge has already pushed the national poverty rate up by roughly 8 percentage points, with a recent survey by the Power and Participation Research Centre (PPRC) estimating current poverty at 26.7 percent. Around 8 percent of household income is now spent solely to cope with higher food costs.

This straitened condition is quite evident from the queue of customers at Bangladesh Bank in Dhaka for withdrawal or encashing saving certificates before maturity or collecting interest just to keep their household afloat. Many savers are liquidating investments rather than making new ones.

We are in accord with the economists, who warn that this savings depletion trend reflects a deeper income crisis. The interplay of high inflation, stagnant wages, and declining trust in banks is creating a vicious cycle. When households use up or deplete savings to meet daily expenses, national investment capacity suffers, slowing economic growth. According to former World Bank lead economist Dr. Zahid Hossain, when wages stagnate and prices rise, people cannot save, rather they are forced to use whatever savings they have for urgent needs. Even with higher interest rates, if income does not increase, savings will decline.

Meanwhile, the government has lowered interest rates on national savings certificates to maintain macroeconomic stability. This decision, however, has hurt retirees and others who depend on savings profits to defray the monthly expenses. When income falls, people usually reduce consumption; but this is dangerous, warn economists. BBS notes that GDP growth has slowed and under-employment has risen since the pandemic, further squeezing household finances. With wages declining to keep pace with prices, costs are rising twice and breaking savings has become too frequent for survival.

Households are now adjusting by cutting protein intake, delaying medical care or reducing education expenses. Government relief measures including TCB goods sale from truck at subsidized prices at different time to curb inflation provided only temporary respite. More sustained support is needed. While some rural social safety programmes exist, urban residents receive little protection. Economists emphasise that stabilising food prices, boosting employment and ensuring reliable social protection would help restore confidence in formal savings instruments. The authorities have to address inflation properly, or else many of their achievements are likely to go in vain.